12. Variance of 2 stocks part 1

M4 L2A 08 Variance Of 2 Stocks Part 1 V3

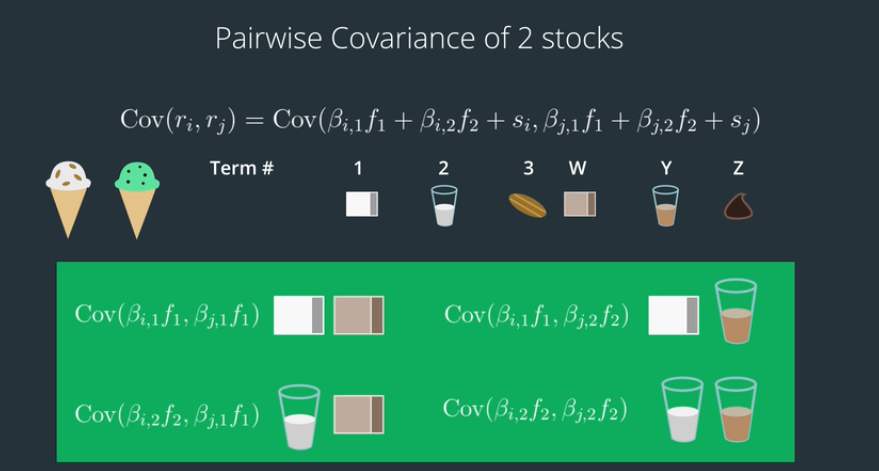

Covariance of 2 stocks

The covariance of two stocks can be written as the sum of the covariances of the factors. In this example we have two factors, so we have four covariance terms. If we were using three factors to describe the asset returns, there would be three times three or nine covariance terms.